Manufacturing Activity Worldwide Jumped in May, Spurred by Stronger Demand Across Major Economies, Indicating Robust Outlook for H2 2024: GEP Global Supply Chain Volatility Index

- Index breaks into positive territory for the first time in 14 months as global manufacturers report stretched capacity

- Demand for raw materials, commodities and components accelerates, a positive indicator for the rest of 2024

- Factory purchasing in Asia rising at the fastest rate since December 2021, driven by India, China and South Korea

- Slack in European markets rapidly shrinking, indicating an advancement of the region’s manufacturing recovery

- Global reports of order backlogs rising because of staff shortages at their highest since late 2022, signaling future price pressures

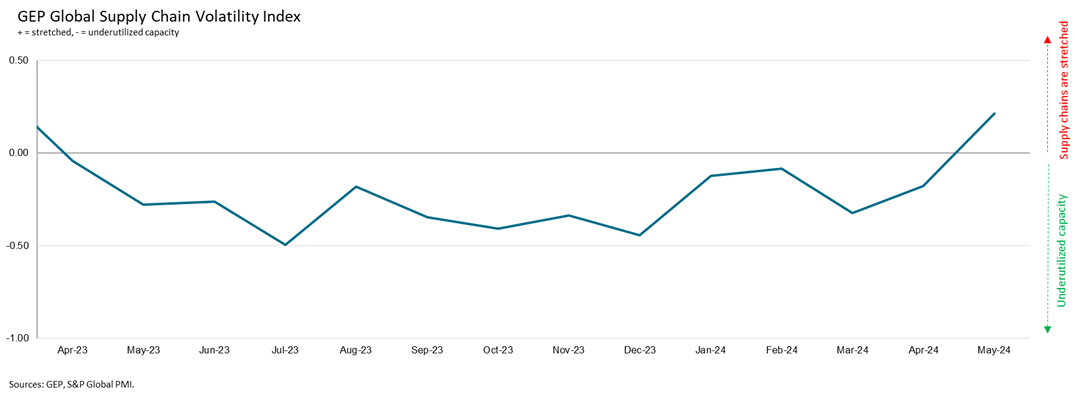

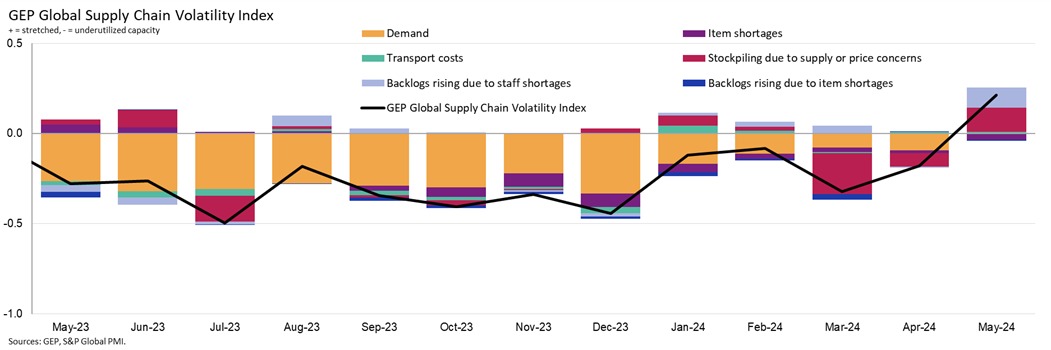

Clark, N.J., June 13, 2024 – The GEP Global Supply Chain Volatility Index — a leading indicator tracking demand conditions, shortages, transportation costs, inventories and backlogs based on a monthly survey of 27,000 businesses — increased notably in May to 0.21, from -0.18 in April. Crucially, this was the first time since March 2023 that the index is in positive territory, signaling that global vendors are working at capacity and that supply chains are at their busiest for more than a year.

Interpretating the data:

- Index > 0, supply chain capacity is being stretched. The further above 0, the more stretched supply chains are.

- Index < 0, supply chain capacity is being underutilized. The further below 0, the more underutilized supply chains are.

A key factor behind the index’s increase in May was a further improvement in global manufacturing demand, leading factories to ramp up their purchases of raw materials, commodities and components. Purchasing growth was especially strong in Asia, particularly in key exporting countries such as China, India and South Korea.

Suppliers to North America also got busier during May, with their capacity slightly stretched as a result. This partly reflected more supportive demand conditions for businesses in the U.S. and Mexico. The European market, which has been a laggard since mid-2022, improved notably, especially in the U.K.

Globally, reports of backlogs increasing because of staff shortages at suppliers of critical goods and inputs hit their highest in almost a year-and-a-half in May, suggesting capacity expansion is required to meet existing and future orders. Overall, this paints an optimistic picture for the outlook in H2 2024 for global supply chains.

“The broad-based nature of the breakout we’re seeing in May is a hugely encouraging sign for the global economy going into the second half of 2024,” explained Mudit Kumar, vice president, GEP Consulting. “If this trend continues, businesses can expect renewed efforts by vendors to raise prices, especially given the recent surge in the cost of many commodities.”

MAY 2024 KEY FINDINGS

- DEMAND: Global demand for raw materials, commodities and components is now trending in line with its long-term average, indicating that global manufacturing is now moving toward an upswing in the business cycle. At the forefront of growth is Asia, led by China, India and South Korea.

- INVENTORIES: The inventory cycle has stabilized, with firms neither building up stocks excessively nor aggressively destocking to improve cash flow and cut costs.

- MATERIAL SHORTAGES: Global item supply remains robust, with reports of shortages at low levels.

- LABOR SHORTAGES: The frequency at which global suppliers reported a rise in their backlogs due to labor shortages was at its greatest in nearly a year-and-a-half, indicating that capacity expansion is required to sustainably meet current and future demand.

- TRANSPORTATION: Global transportation costs remain stable, close to historically typical levels.

REGIONAL SUPPLY CHAIN VOLATILITY

- NORTH AMERICA: Index rose to 0.09, from -0.30, its highest since February. May data showed stronger demand from manufacturers in the U.S. and Mexico, exerting more pressure on North American suppliers.

- EUROPE: Index rose to -0.13 from -0.55, a 14-month high and signaling a substantial reduction in slack across Europe’s supply chains. This suggests the region’s manufacturing downturn continues to recede.

- U.K.: Index rose to 0.15, from -0.47. This showed increased capacity pressures at U.K. suppliers for the first time since January 2023.

- ASIA: Index rose to 0.19, from 0.07. Suppliers to Asia are the busiest globally because of particularly strong demand pressures arising from major markets such as China, India and South Korea.

For more information, visit www.gep.com/volatility

Note: Full historic data dating back to January 2005 is available for subscription. Please contact economics@spglobal.com.

The next release of the GEP Global Supply Chain Volatility Index will be 8 a.m. ET, July 12, 2024.

About the GEP Global Supply Chain Volatility Index

The GEP Global Supply Chain Volatility Index is produced by S&P Global and GEP. It is derived from S&P Global’s PMI® surveys, sent to companies in over 40 countries, totaling around 27,000 companies. The headline figure is a weighted sum of six sub-indices derived from PMI data, PMI Comments Trackers and PMI Commodity Price & Supply Indicators compiled by S&P Global.

- A value above 0 indicates that supply chain capacity is being stretched and supply chain volatility is increasing. The further above 0, the greater the extent to which capacity is being stretched.

- A value below 0 indicates that supply chain capacity is being underutilized, reducing supply chain volatility. The further below 0, the greater the extent to which capacity is being underutilized.

A Supply Chain Volatility Index is also published at a regional level for Europe, Asia, North America and the U.K. For more information about the methodology, click here.

About GEP

GEP® delivers AI-powered procurement and supply chain solutions that help global enterprises become more agile and resilient, operate more efficiently and effectively, gain competitive advantage, boost profitability and increase shareholder value. Fresh thinking, innovative products, unrivaled domain expertise, smart, passionate people — this is how GEP SOFTWARE™, GEP STRATEGY™ and GEP MANAGED SERVICES™ together deliver procurement and supply chain solutions of unprecedented scale, power and effectiveness. Our customers are the world’s best companies, including more than 550 Fortune 500 and Global 2000 industry leaders who rely on GEP to meet ambitious strategic, financial and operational goals. A leader in multiple Gartner Magic Quadrants, GEP’s cloud-native software and digital business platforms consistently win awards and recognition from industry analysts, research firms and media outlets, including Gartner, Forrester, IDC, ISG, and Spend Matters. GEP is also regularly ranked a top procurement and supply chain consulting and strategy firm, and a leading managed services provider by ALM, Everest Group, NelsonHall, IDC, ISG and HFS, among others. Headquartered in Clark, New Jersey, GEP has offices and operations centers across Europe, Asia, Africa and the Americas. To learn more, visit www.gep.com.

About S&P Global

S&P Global (NYSE: SPGI) S&P Global provides essential intelligence. We enable governments, businesses and individuals with the right data, expertise and connected technology so that they can make decisions with conviction. From helping our customers assess new investments to guiding them through ESG and energy transition across supply chains, we unlock new opportunities, solve challenges and accelerate progress for the world. We are widely sought after by many of the world’s leading organizations to provide credit ratings, benchmarks, analytics and workflow solutions in the global capital, commodity and automotive markets. With every one of our offerings, we help the world’s leading organizations plan for tomorrow, today.

Media Contacts

| Derek Creevey Director, Public Relations GEP Phone: +1 732-382-6565 Email: derek.creevey@gep.com |

Joe Hayes Principal Economist S&P Global Market Intelligence Phone: +44-1344-328-099 Email: joe.hayes@spglobal.com |

Disclaimer

The intellectual property rights to the data provided herein are owned by or licensed to S&P Global and/or its affiliates. Any unauthorised use, including but not limited to copying, distributing, transmitting or otherwise of any data appearing is not permitted without S&P Global’s prior consent. S&P Global shall not have any liability, duty or obligation for or relating to the content or information (“Data”) contained herein, any errors, inaccuracies, omissions or delays in the Data, or for any actions taken in reliance thereon. In no event shall S&P Global be liable for any special, incidental, or consequential damages, arising out of the use of the Data. Purchasing Managers’ Index™ and PMI® are either trade marks or registered trade marks of S&P Global Inc or licensed to S&P Global Inc and/or its affiliates.

This Content was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global. Reproduction of any information, data or material, including ratings (“Content”) in any form is prohibited except with the prior written permission of the relevant party. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content.